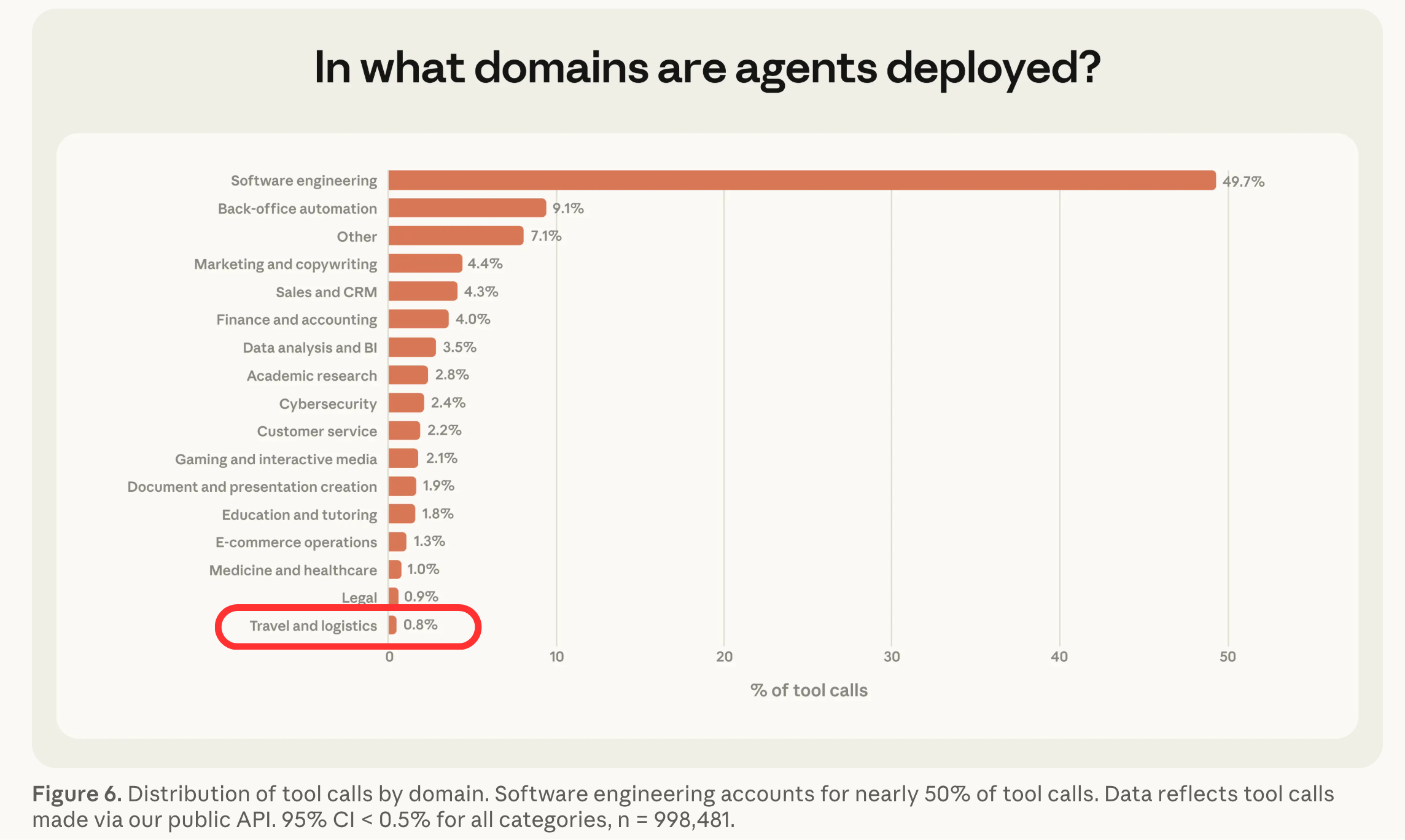

According to Anthropic’s February 2026 analysis, travel and logistics rank last in agentic AI penetration, representing just 0.8% of “tool calls”—the measurable instances where AI systems take action inside real operational software, not just generate text—compared to nearly 50% for software engineering. For an industry that contributes nearly $12T to global GDP, this gap is one of the most underappreciated opportunities in enterprise AI.

The High Cost of Technology Maintenance

Travel organizations carry a burden of technical debt that is uniquely visible compared to other sectors. For example, while financial services also grapples with legacy infrastructure, the industry has successfully built digital wrappers (such as Zelle and mobile apps) that insulate the consumer from 60-year-old COBOL code hiding underneath.

In travel, there is no such insulation. When a legacy system fails, thousands of passengers are stranded in terminals and aircraft are grounded on the tarmac. While a banking glitch might delay a digital transfer, a legacy airline IT failure costs the industry roughly $400,000 per hour in direct downtime. Total flight disruptions now cost the global airline industry roughly $60 billion annually.

And the cost isn’t limited to downtime. It compounds upstream into revenue. Post-COVID, loyalty programs, ancillary revenue, and direct booking relationships have become among the most powerful differentiators; the carriers that pulled ahead did so by owning the customer relationship end-to-end. Airlines are chasing a $145 billion ancillary revenue market, but they are trying to capture it using systems that view a passenger as a 'Record Locator' rather than a customer. This legacy architecture makes dynamic bundling and real-time offer management, the two pillars of modern ancillary revenue, nearly impossible for many.

The result is that the same technical debt constraining operational day-to-date performance is also capping the revenue ceiling. In an industry with $1 trillion in annual revenue, technology debt represents a $30-60 billion annual constraint on growth. Aviation is a business of thin margins, where profit is measured in single digits. Investing in new technology is the primary lever for protecting operational efficiency and capturing revenue.

Rewriting the Build-vs-Buy Calculus

Historically, the barrier to proprietary travel tech was not just the cost of talent. It was also the opacity of legacy codebases that made the ROI on building internally almost impossible to clear.

United Airlines provides a lesson in architectural will. Starting in 2018, CEO Scott Kirby invested hundreds of millions of dollars to dismantle a 1960s-era Fortran mainframe. While the decision may have seemed "irrational" from a short-term budgetary perspective, the overhaul now allows United to process refunds and manage complex disruptions within its mobile app, automatically reaccommodating passengers in minutes (versus competitors who take hours to days). This reduces the downstream cost of irregular operations and wins over loyal customers along the way.

But AI has not made building a universal mandate. Even for Tier 1 carriers, internal development is a surgical decision based on a ruthless assessment of where proprietary data creates an insurmountable advantage and where it does not.

Large carriers will build where data is a unique asset and coordination is entirely internal — personalization engines, crew rostering, back-office automation, customer service against their own booking data. No vendor can build a better version of these systems because no vendor has access to the operational logic and data that makes each carrier distinct. They will buy where workflows cross organizational boundaries by definition — ATC coordination, codeshare and interline settlement, airport turn management, flight dispatch, customs compliance. These are ecosystem problems that no single carrier can solve unilaterally.

The boundary between what carriers will build and what they can’t is the most important bright line in travel technology today. Everything on the coordination side of that line is a startup opportunity, and notably, one that serves the entire market, because the value of a neutral third-party orchestrator increases with every carrier that adopts it.

The Startup Advantage: The Orchestration Layer

AI startups can serve as that orchestration layer. Picture this: every flight involves dozens of sequential handoffs, starting with gate assignments confirmed with the airport, fuel orders placed with suppliers, ground handling crews dispatched, cargo manifests filed with customs, slot times coordinated with air traffic control...the list goes on. And each handoff is a potential failure point. Many of these are still managed through manual processes, like phone calls. Fax machines and batch file transfers were state-of-the-art in 1995, and haven’t been updated since.

No single airline can solve it unilaterally because the friction lives between organizations, not within them. Incumbents are structurally incentivized to protect data silos; startups are structurally incentivized to build the orchestration layer that sits across them.

Startups can win by building what we call "Systems of Action," or systems that autonomously execute across organizational boundaries. A System of Action doesn't alert an operations manager of a ground delay program; it uses AI to simultaneously rebook 200 passengers across three carriers, trigger ground handler reassignments, file the regulatory notifications, and update the cargo manifest, all without human intervention. That is a categorically different product from anything incumbent vendors offer today.

In a heavily regulated environment, the natural objection to autonomous cross-party decision-making is accountability: who is responsible when an AI system makes a consequential call affecting multiple organizations? The answer is the audit trail, and here the regulatory burden becomes a product advantage. A startup that can provide an immutable, AI-generated record of every autonomous decision, every party notified, and every regulatory requirement satisfied is building the trust infrastructure. The compliance layer isn't the cost of doing business. It's the moat.

A Call for Builders

Building in travel is hard for one reason above all others: access. Access to airlines willing to pilot new technology. Access to airports willing to share data. Access to OEMs willing to co-develop. That access is exactly what SKY VC offers. Our 100+ strategic partners are the industry, and over half of our portfolio companies generate revenue from introductions we made.

The holding pattern is over. We’re looking for the founders who know it.

.jpeg)